‘Fire In Paradise’ Shows How Risk Happens Fast

Submitted by Silverlight Asset Management, LLC on November 16th, 2019

It started out like any small fire. Then it spread.

Fire in Paradise is a new Netflix documentary about the 2018 fire that eviscerated the small town of Paradise, California. The film chronicles the moment-to-moment drama of how the most devastating wildfire in over a century unfolded. You learn about brave firefighters who risked their lives to save lives, heroic teachers, and everyday people trying to persevere in the aftermath of it all.

Here’s the official trailer:

The film prompted my wife and I to discuss our fire safety plan. As California residents, we’re not immune to the risk.

Later, the film also made me think of a market-related analogy.

The Relationship Between Risk and Liquidity

Nothing that transpires in markets compares to the tragedy fire victims face. Fire can be a useful analogy, though, because it’s a primal risk everyone understands.

If you see a fire coming, the danger is obvious. The immediate instinct is to run away, and that’s the correct action.

Investment risks are different. They can be hard to spot, even in plain sight. Also, by the time everyone notices a risk, it usually pays to run toward the fire.

Real fires and “market fires” are similar in how they can both happen fast.

The initial spark for the Camp Fire that ravaged Butte County last year was a faulty transmission line. From there, a combination of high winds, high temperatures, and parched vegetation from a drought, made a conducive environment for the fire to rapidly spread.

As the fire made its way toward the town of Paradise, residents scrambled to evacuate. The roadways could not handle so many people leaving at once, however. Traffic jams ensued. Soon, many were helplessly stuck in the middle of the fire.

There’s a market adage: “Risk happens fast.”

Macro risks usually start out festering in the shadows, until a tipping point arrives. After the threat becomes evident to the masses, a stampede commences.

In a market dislocation, the “blocked roadway” is a liquidity shortage. There aren’t enough buyers to absorb the sudden influx of sellers, so prices plummet.

We don’t need to identify the precise spark that ignites a market fire. But we do want to stay vigilant monitoring for conditions that create a ripe atmosphere for a market event.

Currently, there’s a high-profile town in Northern California at risk.

What if a fire has already started in Silicon Valley?

The last cycle was a real estate/finance boom. Years of easy money inflated real estate to irrational heights.

This cycle’s main catalyst is a tech/consumer boom, where prolonged monetary easing has once again caused assets to soar to irrational heights.

In fact, many of today’s market darlings trade at similar valuations as the Nifty 50 stocks from the early 1970s. For those who don’t know, that was one of the classic stock market bubbles of all-time.

Source: INTL FCSTONE

The 'Nifty 50' was a group of popular, “one-decision stocks.” Many were tied to the Baby Boom Generation coming of age as consumers.

Modern tech giants like Netflix and Amazon are also riding a demographic tailwind. Millennials fueled the ascent of these companies.

Along the way, Silicon Valley became a unique “paradise” in this market cycle. A magical place where the sun always shines, stock options go to the moon, and companies build office complexes resembling space ships.

Apple Campus in Sunnyvale, CA. Source: Getty Images

But smoke is now emanating from the valley. And there are plenty of catalysts that could help the fire spread.

Peak growth. Netflix’s subscriber count fell for the first time in Q2 2019. And that was before new competing services like Disney+ and Apple TV+ launched.

Overall sales for the FANGs are growing. But the gap in their combined growth rate compared to the rest of the market is at the lowest level this cycle.

Peak performance. When growth peaks, performance suffers.

Did you know Netflix, Amazon, Facebook and Google have all underperformed the S&P 500 since the summer of 2018?

In recent months, growth stocks have broadly lagged the market. It might be a small fire so far, but it started on the heels of growth stocks reaching their highest valuation premium since the dot-com bubble, and we know how that ended.

Private market valuations. The way Silicon Valley operates, every private market company’s valuation is based off someone else’s valuation. So, when a major unicorn like WeWork stumbles at the IPO gate, and has to mark down its valuation substantially, there’s a domino effect.

This isn’t terribly different from what transpired between 2006- 2008. After subprime mortgage defaults picked up, illiquid bundles of mortgages (i.e. CDOs) had to be marked-to-market. Once a negative feedback loop like that starts, it can be tough to reverse.

Failed IPOs. WeWork may turn out to be the “Pets.com” of this cycle, but it isn’t the only failed IPO this year.

Recall Uber’s IPO back in May? The shares started out around $45. Today, the stock is at $26.70.

Yet, even after a 40% haircut, Travis Kalanick still doesn’t appear bullish on the company he co-founded. The former-CEO just sold over a half a billion dollars worth of stock last week.

Lyft traded over $75 after going public in March. Now it trades around $42.

Pinterest surged after its IPO. But the stock is down 40% since August, leaving a volatility scar that may deter future investors.

IPOs are an exit ramp for VCs to monetize their early-stage investments. As that window gets tighter, it breeds more risk aversion in the Valley, contributing to a negative feedback loop.

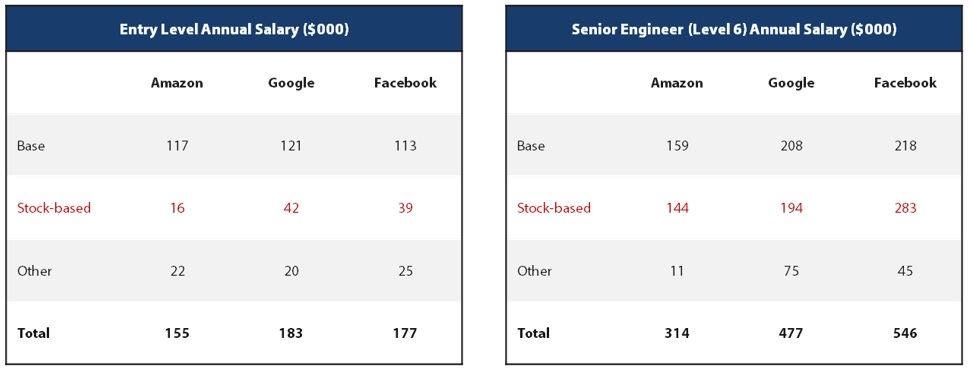

Stock-based compensation. Vincent Deluard is a macro strategist at INTL FCStone. He recently completed an excellent interview with RealVision, and has done interesting work on the outlandish growth in stock-based compensation at Bay area firms.

Ever wonder how much people working at Amazon, Google, and Facebook earn? If you know where to look, you can estimate it.

Level.fyi is a website that crowdsources compensation data to help engineers contemplate offers from big tech companies. Mr. Deluard recently ran the numbers on compensation for entry-level engineers and senior engineers with around 10 years experience.

Sources: Level.fyi, INTL FCStone

Stock-based comp accounts for roughly half of the total payout for senior engineers, and about a quarter of the total pay for entry-level engineers.

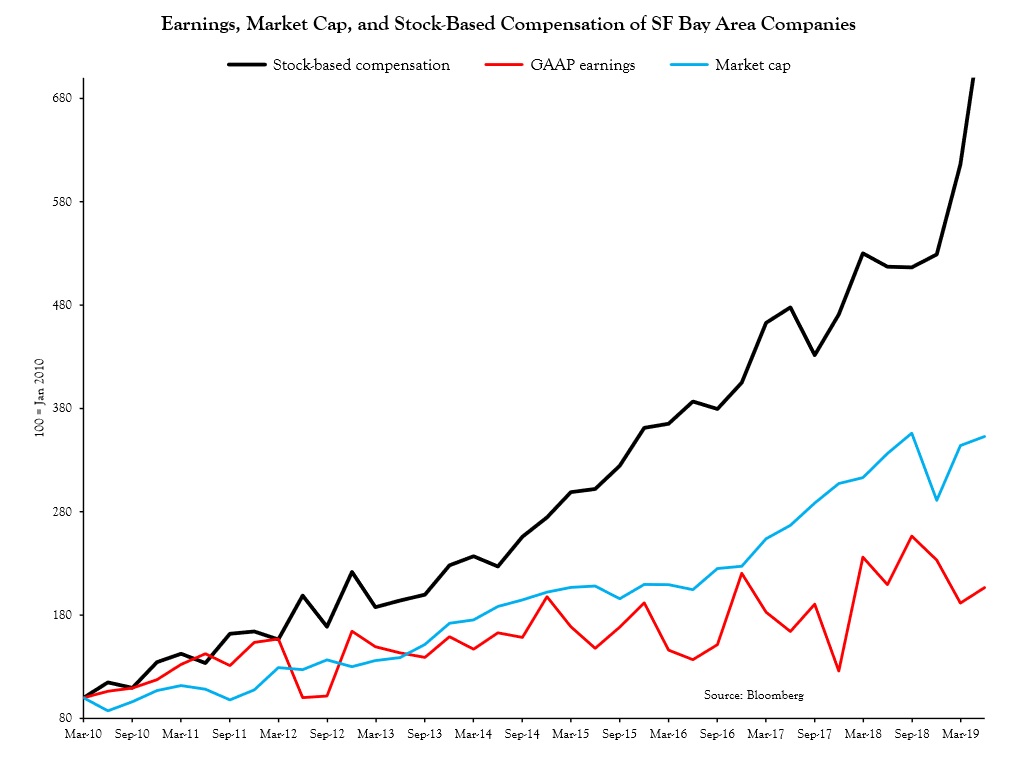

These numbers are part of a broader story. By Mr. Deluard’s math, overall stock-based comp at 276 Bay Area firms he tracks rose almost eight-fold since 2010, dramatically outpacing market cap appreciation and earnings growth.

The chart below demonstrates the unsustainable nature of the current model. “You would need an infinite amount of growth to sustain these practices,” he says.

Source: INTL FCSTONE

Outsourcing a huge portion of their compensation expense to the stock market frees up cash for tech firms to invest in growth projects, or cut prices to gain market share.

Problem is, this becomes a house of cards if the stocks cease going up.

Real estate. A boom in venture capital and the long equity bull market have led to rapid appreciation in Bay Area real estate. Until recently, that is.

The Case-Shiller Index of national home prices is still rising, yet San Francisco peaked in September 2018. Interestingly, that was around the same time the FANGs started underperforming.

Positioning. Finally, it’s always important to consider investor positioning.

One thing that made Paradise vulnerable to a fire was the town’s population density. This wasn’t a tiny community of folks spread out in the woods. Rather, it was a town of more than 26,000 close nit neighbors, whose population density was 520% higher than the California average and 1491% higher than the national average.

This explains why the roads got so jammed when everyone tried to leave.

This explains what made the whole affair so treacherous.

Crowded trades are how “population density” manifests in the market. According to Bank of America Merrill Lynch’s latest global survey, being long U.S. tech and growth stocks qualified as the most crowded trade among 178 fund managers surveyed.

Originally published by Forbes. Reprinted with permission.

This material is not intended to be relied upon as a forecast, research or investment advice. The opinions expressed are as of the date indicated and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by Silverlight Asset Management LLC to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Silverlight Asset Management LLC, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any of these views will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Testimonials Content Block

More Than an Investment Manager—A Trusted Guide to Financial Growth

"I’ve had the great pleasure of having Michael as my investment manager for the past several years. In fact, he is way more than that. He is a trusted guide who coaches his clients to look first at life’s bigger picture and then align their financial decisions to support where they want to go. Michael and his firm take a unique and personal coaching approach that has really resonated for me and helped me to reflect upon my core values and aspirations throughout my investment journey.

Michael’s focus on guiding the "why" behind my financial decisions has been invaluable to me in helping to create a meaningful strategy that has supported both my short-term goals and my long-term dreams. He listens deeply, responds thoughtfully, and engages in a way that has made my investment decisions intentional and personally empowering. With Michael, it’s not just about numbers—it’s about crafting a story of financial growth that has truly supports the life I want to live."

-Karen W.

Beyond financial guidance!

"As a long-term client of Silverlight, I’ve experienced not only market-beating returns but also invaluable coaching and support. Their guidance goes beyond finances—helping me grow, make smarter decisions, and build a life I truly love. Silverlight isn’t just about wealth management; they’re invested in helping me secure my success & future legacy!"

-Chris B.

All You Need Know to Win

“You likely can’t run a four-minute mile but Michael’s new book parses all you need know to win the workaday retirement race. Readable, authoritative, and thorough, you’ll want to spend a lot more than four minutes with it.”

-Ken Fisher

Founder, Executive Chairman and Co-CIO, Fisher Investments

New York Times Bestselling Author and Global Columnist.

Packed with Investment Wisdom

“The sooner you embark on The Four-Minute Retirement Plan, the sooner you’ll start heading in the right direction. This fun, practical, and thoughtful book is packed with investment wisdom; investors of all ages should read it now.”

-Joel Greenblatt

Managing Principal, Gotham Asset Management;

New York Times bestselling author, The Little Book That Beats the Market

Great Full Cycle Investing

“In order to preserve and protect your pile of hard-earned capital, you need to be coached by pros like Michael. He has both the experience and performance in The Game to prove it. This is a great Full Cycle Investing #process book!”

-Keith McCullough

Chief Executive Officer, Hedgeye Risk Management

Author, Diary of a Hedge Fund Manager

Clear Guidance...Essential Reading

“The Four-Minute Retirement Plan masterfully distills the wisdom and experience Michael acquired through years of highly successful wealth management into a concise and actionable plan that can be implemented by everyone. With its clear guidance, hands-on approach, and empowering message, this book is essential reading for anyone who wants to take control of their finances and secure a prosperous future.”

-Vincent Deluard

Director of Global Macro Strategy, StoneX